If you have money with a financial advisor OR are looking to invest with one…

My brand new book reveals:

The 5-Minute Method I Used To Become A Millionaire In The Stock Market In Just 5 Years

While sitting on the toilet each morning

All without:

Having to be an expert in the markets…

All without:

Spending all day staring at screens and graphs…

All without:

Or taking crazy risks (in fact I have NEVER lost money in the stock market!)

My name is Ryan Cramer

In fact, my investing has recently allowed me to leave America and live ‘The Freedom Lifestyle’ in Thailand, as you can see:

And you’re an American who has money in the hands of a financial advisor…

OR you have money you’re wanting to invest, but have no idea who to trust with it…

I’m going to show you why you need to STOP letting banks and financial advisors steal from you and how it’s possible for YOU to quickly and easily manage your own money and investments in less than 5 minutes per day.

In fact, I’m going to show you how it’s possible to easily get a return that’s 5-7x HIGHER than any financial advisor could ever DREAM of…

By simply buying proven stocks that are having a ‘bad day’.

I’m going to show the exact method I been quietly using to gain a 66% increase on my investments, every single year.

And why the average employed American can make an automatic 22% increase by simply and easily managing their own money.

Without constantly having to study the markets…

Without needing to learn complicated trading strategies…

Without gambling on penny stocks…

And without having to become a trading expert.

And I’m going to show you how I did it.

But first...

Why the hell should ANYONE manage their own money instead of just letting qualified financial advisors take care of it?

They serve no purpose but to steal people’s money, and convince the general public they should be happy with measly 3-5% annual returns on investment.

If there’s an 8th circle of hell, it’s reserved for financial advisors.

At this point, my friends know just not to bring up the subject around me.

Especially not when they want to have a good night out.

And here’s why:

A decade or two ago, I trusted financial advisors.

Like many people, I believed they could do no wrong.

Believed that if I just left my money in their magical hands, it would someday turn into retirement money.

It’s what my parents believed.

It’s what my friends believed.

And so… it’s what I believed.

I trusted those fuckers blindly.

And before you call me ‘harsh’ for using that kind of language…

Let me make a note here and say that my BEST FRIEND was a financial advisor.

And I trusted him too.

And when I got married in 2000, I gave this best friend financial advisor ALL our collective gift money.

Some $8,000 dollars in all.

I thought we were being responsible.

I thought:

And by the time I paid my financial advisor’s fees etc., my money was making me 4% a year.

Sometimes 5%.

But not much more.

And then a few years later, I got a phone call...

“What do you mean GONE?!”

“It’s gone Ryan. I’m really sorry. I did my best.”

I stared at the phone in disbelief.

GONE?! HOW?!

$8,000 is a fair bit of money!

Wondering how on earth these people could get away with blind robbery.

Then two things happened at once.

The 2008 crash started… and my wife and I got divorced.

(and before you go feeling sorry for me – don’t. I’m not here to give marriage advice. That shit is WAY harder than investing in the stock market)

Anyways.

We split up, the housing market crashed… and I was left nearly homeless and sleeping on my friend’s couch.

I had almost nothing to my name, AND I was on the hook for 10 years of child support.

And between trying to get my life together and pay alimony…

I didn’t have much time or money to get into the stock market.

(every extra penny was going to support my ex-wife and kids anyways).

Between 2008 and 2017, I did almost zero investing.

I just didn’t have the time or money for it.

I did, however, get my financial services license and pass my Series 7, Series 66, and life insurance & health insurance exams.

I figured it would be the best way to break into the financial advisor’s world and see just how everything worked.

And what I uncovered was actually

PRETTY SHOCKING!

See – I always thought that financial advisors were super smart, stock-savvy people.

I thought that investing money was something super complicated that only cutting-edge Wall Street Boys could do.

You know.

Frantic phone calls and everybody yelling across cigarette smoke-filled rooms.

Crazy charts and all sorts of inside information.

But when I started looking into it…

They rolled into work 17 minutes late.

They took a 2-hour corporate-sponsored lunch.

They left work at 4:02pm.

And above all, they REALLY didn’t seem to care about the money they were managing.

They didn’t care about the retirement funds, education funds, or the life savings they had been trusted with.

And when I started looking at their ACTUAL workplaces and hiring practices…

(and how they got paid…)

I realized it was NO WONDER financial advisors really REALLY didn’t care.

Half the time, these guys were on FLAT SALARIES!

Which meant it didn’t matter whether they did a good or bad job with my money…

They STILL GOT PAID!

But it gets worse.

It turns out, these financial advisor chumps are usually incentivized to push mutual funds with abysmal returns.

In other words, they get a kickback from selling you on some shitty mutual fund!

And rather than actually building individual portfolios for people, they usually just invest in mutual funds (which are communal funds with a lot of people’s money and stocks all jammed together).

But here's the problem:

Mutual Funds are subject to Capital Gains tax

And when you’re a part of a mutual fund…

You pay Capital Gains tax on stocks that go up in value… even if your stocks go DOWN in value.

Which is basically how my financial advisor ‘friend’ ended up losing all of my money.

He bought stocks inside mutual funds that ended up LOSING me money…

AND THEN I had to pay taxes on other stocks in that mutual fund that went up in value…

So I was losing money having someone else manage my money in a mutual fund…

I was being taxed on stocks I didn’t own…

AND my financial adviser was STILL taking a cut while he rode my account into the ground.

He sold me into a mutual fund that was a terrible idea…

He had no incentive to actually make me money…

I got charged Capital Gains tax on things I didn’t own…

And he kept his job while I lost $8,000 dollars that were supposed to set my wife and me up for our new life.

That’s the point when I realized a hard truth…

No one else cares about your money.

In other words…

No one was going to care about my money as much as I did

I WAS DAMN WELL GOING TO LOSE IT MYSELF!

And at this point it was 2017, nearly a decade after the 2008 crash.

My alimony payments were done.

My wife/ex-wife wasn’t spending all my money.

And I FINALLY had some resources to start investing with.

So I took what I had learned as a financial advisor…

But I used it to manage my own stocks inside a 401K.

(Sounds complicated, but it’s not. It’s a single piece of paper you can file online.)

That first year, I made a 66% increase on my stocks…

And the first 22% I made automatically without risking a penny.

See, because I was in the 22% tax bracket…

(and a 401K is an account that lets you invest PRE-TAX dollars instead of putting after-tax dollars in a mutual fund)…

Every dollar I put into a 401K was automatically worth $1.22.

That’s a 22% increase instantly.

Then I bought stocks that were just slightly, SLIGHTLY more aggressive than most mutual funds…

And I was well on my way to my 66% increase.

And because my employer at the time would MATCH my contributions to my 401K…

I doubled my money really quickly.

But Ryan, you might be thinking, if you were able to get those returns so easily… why don’t financial advisors do the same?

Good question.

And I’ll tell you why.

It’s because financial advisors have what I call a '3 condoms mentality' - if one condom works well, 3 condoms must work 3 times as well, right?

And I mean that almost literally.

They are some of the softest, most risk-averse bone-headed mediocre humans on the planet.

They want SAFE.

Like SUPER SAFE.

If it was up to them, we’d have 6-point racecar harnesses on buses.

We’d cover ourselves in bubble wrap when riding bikes.

And we’d wear two life jackets when it rains.

They simply have ZERO risk tolerance at all.

So they can seal their 2-3% fees and keep their jobs and leave you with 4-5% returns on a good year.

And because most people think that investing is really tricky…

AND would rather see a TINY return than risk any kind of loss…

Financial advisors keep their jobs.

And I'm going to be completely clear here...

Or you want to live in a white padded room your whole life and just get by…

You can stop reading here.

This isn’t for you.

This is for people who are ok with taking a slightly more aggressive route and having it pay off.

TO BE CLEAR.

I’m not suggesting big risks here. Nothing unreasonable.

(I still wear a helmet when riding a bike after all).

For this to work, you have to be just slightly more aggressive than what most financial advisors have the balls for.

Which is exactly what I did.

And it was perfect.

I didn’t want to ‘day trade’…

I didn’t want to spend hours pouring over screens and listening to financial podcasts…

And I definitely didn’t want to do anything too aggressive or risky.

I just wanted a simple and proven way to manage my own money quickly, and then get on with my life.

So I developed a set of stock-finding filters…

And came up with a method for buying stocks that I was almost certain would grow quickly.

And pretty soon I was able to consistently get returns each month that my financial advisor used to get for me each year!

I was getting 4-5% returns PER MONTH instead of per year.

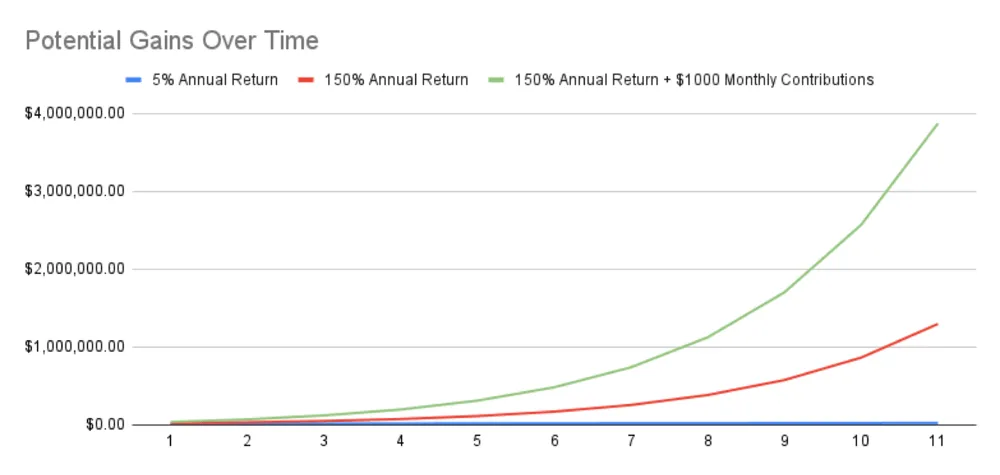

Take a look at the graph below:

The BLUE line shows what would happen with a 5% annual return.

(Which is what you can expect to make with a financial advisor after they take their 2-3% fee)

After 11 years, your money would have turned in $25,655…

(And your financial advisor will have taken $5,916 from you)

The RED line shows what would happen with a 50% annual return.

(which is less than the 66% annual increase I’ve been able to get, but still WAY ahead of any financial advisor or mutual fund).

After 11 years of a 50% annual return, your money would have turned into $1,297,463!

That’s nearly $1.3 MILLION dollars instead of $26k.

And if you invested $15k using my strategies…

And contributed $1,000 a month…

AND were able to make 50% returns per year…

The GREEN line shows that you’d be a millionaire in just 8 years, and have $3,870,807 after 11 years!

Crazy I know… but that’s how the math works out.

And in fact, it’s EXACTLY what my girlfriend did.

(yeah yeah – I’ve started dating someone new since the beginning of this story… I told you, I’m not the guy to ask for marriage advice).

But back to my girlfriend.

At first, she tried to overcomplicate my system.

She tried to spend more than 5 minutes per day applying my filters to find stocks to buy…

Tried to ‘do more’…

Tried to add in complex strategies…

But after struggling and losing money in the markets for a while, I FINALLY convinced her to commit to my system.

5 minutes per day – no more, no less.

(unless she took a day or two off, in which case she’d just check back when it was convenient).

And all of a sudden, she started seeing huge returns.

And once she trusted my 5-minute filter-checking method…

She started contributing additional money to her portfolio in addition to her stock buying.

That was just a few years ago… and today her account is worth WELL OVER a million dollars.

She’s become a millionaire in the time we’ve been dating – just by using this system!

And here's the beautiful thing about it:

In fact, the more you try to ‘overdo it’… or ‘add things in’…

The worse it works.

It doesn’t involve ‘day trading’…

It doesn’t require ‘shorting’ and making Wallstreet bets…

And you don’t have to be a genius to do it.

It’s a science… but it’s NOT rocket science.

And if you’re smart enough to get a job, and learn to do that job well…

You’re smart enough to use this system.

I mean that.

If you ask any of my friends, they’ll tell you I’m actually a pretty regular dude.

I don’t have a genius IQ, and I’ve never been ‘smart’ by any of the usual metrics.

But I’m a firm believer that if you’re smart enough to make and save money…

Then you’re smart enough to buy stocks.

And if you have a proven system that’s simple and easy to follow…

It’s possible to be a ‘dumb guy’ who makes a killing in the long term.

(most times it’s the really smart guys who fuck things up because they try to overcomplicate things – but that’s a topic for another day).

At this point you're probably wondering...

How EXACTLY does this strategy work?

But first, let’s talk about what this strategy is NOT.

It is NOT a ‘day trading’ strategy.

I hate being glued to a computer all day… and 99% of day traders lose money in the long run.

It is NOT a ‘penny stock’ strategy.

Gambling on unproven penny stocks is… well… gambling.

And I work way too hard for my money to leave things up to chance.

It is NOT a ‘big flashy glamorous’ system.

It's not James Bond 'put my life savings on the roulette wheel'.

This is not a ‘sexy system’.

This method is about boring consistency which adds up FAST over time.

I really don’t want any part of something that involves constant buying and selling.

I also don’t want to have to stay up to date with markets…

Or constantly read the Wall Street Journal.

Have you ever read a financial report?

That shit is DRY. No thank you.

So enough with the preamble Ryan...

How the hell does this actually work?

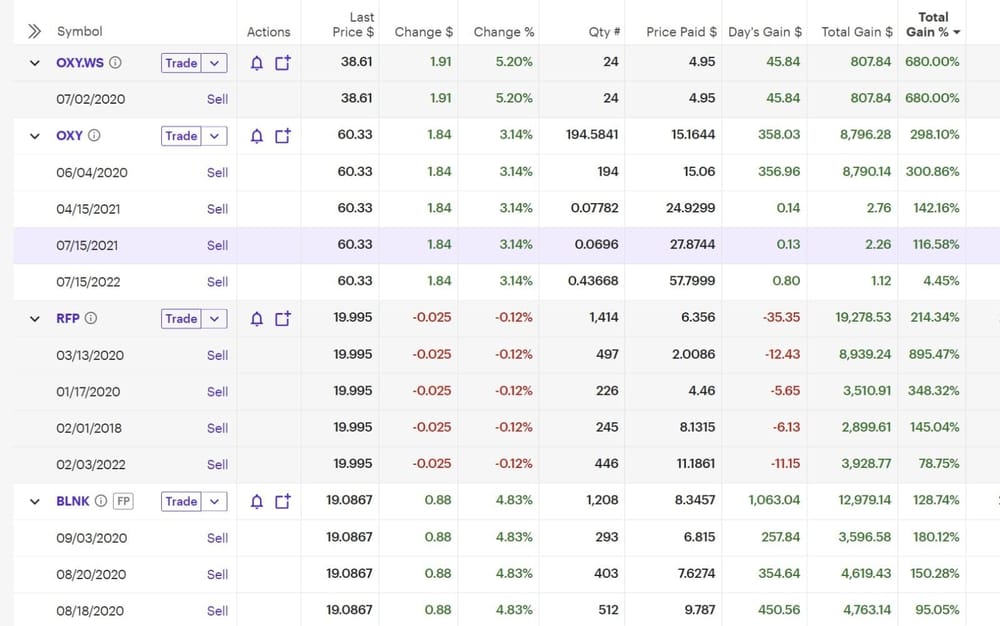

I have a set of proven ‘filters’ and ‘criteria’ for buying stocks.

I developed these filters after seeing what did and didn’t work as a financial advisor…

And tested them with my own money, my girlfriend’s money, and my friend's money.

By using these filters, I’m able to rapidly scan for ‘qualified’ stocks.

These are stocks from companies that are so big and proven that in 3 years, they’re virtually guaranteed to be up.

These stocks are so big that even if they failed, the government would bail their companies out.

Sometimes they’re companies you’ve heard of.

Other times they’re some conglomerate that matches the criteria.

So is that it? Just buy big stocks?

Well no.

Not quite.

See qualified stocks have good days, and they have bad days.

And over 3 years, they’ll almost always go up!

But in the short term, occasionally they have ‘bad days’.

So we want to buy them when they’re having a bad day!

Maybe the Q4 report just came out and the stock is down as a result.

Maybe the CEO just had some sort of personal issue.

Or maybe there was a bad news article about them.

Either way, these ‘bounce back stocks’ are down a little - and virtually guaranteed to go back up!

So if you buy them when they’re ‘on sale’ you’ll be able to capitalize on the short-term rebound AS WELL as the long-term growth.

And because of my ‘5-minute filters’ that I use each morning…

I’m able to easily tell whether the stock is at the bottom of it’s ‘bad day’ or whether it’s going to keep going down or not.

This allows me to quickly and easily buy stocks at the bottom of their ‘bad day’ or ‘bad week’...

And then get an immediate return when they bounce back.

(this is how I’ve been able to get a 66% increase so consistently year over year)

And the best part is, these ‘filters’ allow me to quickly and easily find these ‘bad day’ bounce-back stocks…

Without having to be a financial nerd.

Every day, I run through these filters on my phone while I’m taking my morning dump.

If a stock fits, I buy it.

If two stocks fit, I buy both.

If no stocks fit, I wipe my ass and get on with my day.

That’s it.

My whole system.

Check my filters and criteria, buy if necessary, then rinse and repeat.

If I miss a day, it’s not a problem…

And there is LITERALLY no point in putting in any more effort.

And that’s why this strategy is so incredible.

You can miss a few days, or even weeks, and the system still works.

(you just might miss out on a few juicy bounce-backs)

Which is really helpful, because I’ve moved to Thailand recently, and the internet connection goes down all the time due to storms etc.

I don't have the means or the time to sit there like some trader on the NYSE staring at 15 screens full of graphs moving around constantly.

I don't want to be some 'tech bro' with his phone buzzing all the time with notifications.

I just want to be the guy on the toilet quietly and quickly making a 66% increase every single year while LITERALLY SHITTING on financial advisors.

But that's not even the best part about this strategy...

And here’s why that’s important.

Back in 2017, I was in the 22% income tax bracket.

So the MOMENT I started investing my own money instead of leaving it in some mutual fund…

I make an automatic 22% return because I’m not paying tax on that money!

And if you’re in a higher tax bracket than I was…

Then you can make an even higher immediate return!

But because I was in the 22% tax bracket…

I COULD LOSE UP TO 22% IN THE MARKETS AND STILL BE AHEAD!

I’ve never lost 22%.

Not even once.

Not even during Covid when everything was crashing.

I just found stocks that fit my criteria and bought them when necessary.

Can your financial advisor say the same?

Probably not.

Which just goes to show…

Your money is only safe when YOU are handling it

Ryan - I’m intrigued.

Not entirely convinced, but intrigued.

I get that.

This kind of system…

These kinds of returns…

They’re SO FAR beyond what we’ve been taught to expect in the market.

They seem almost impossible.

But keep in mind…

Those chumps deal with mutual funds so big that they can seek out a 6% annual return.

Steal their 2-3% ‘fee’...

And STILL make a killing for themselves.

But for people like you and I?

We can make WAY MORE MONEY by following a simple system like mine and managing our own money.

So... What's this system going to cost you?

I’m not going to do that.

You’re not my girlfriend or my family…

So you don’t just get complimentary access to it.

If you want access to my filters and 5-minute stock buying strategy…

You’re going to have to pay for it.

Not a lot mind you… but you WILL have to pony up and give me some money.

And before I tell you how much money…

Keep in mind that I don’t make a PENNY off your investments.

So once YOU have the system in YOUR hands…

YOU’LL keep every penny of your returns.

So how much am I charging for my system?

Not nearly as much as it should be.

And if you decide to pull out your credit card TODAY so you can get access to a proven system and take back control of your finances…

I'll Give You The WHOLE System For $27

A whole $27 dollars.

Why just $27?

Well that’s a good question.

This book and proven system are quite frankly worth thousands of dollars.

In the past, I’ve sold this 52 page book outlining my exact strategy for $997…

And it only had half as much stuff in it.

So assuming the system works…

Why on earth would I, the creator, want to practically give it away for $27?

A couple of reasons.

The first reason - and I realize this is going to make me sound like a dick…

Is because I’ve already made enough money to live happily for the rest of my life.

My portfolio has now gotten so big and makes me so much money…

I’m content to just manage my own money each and every morning,

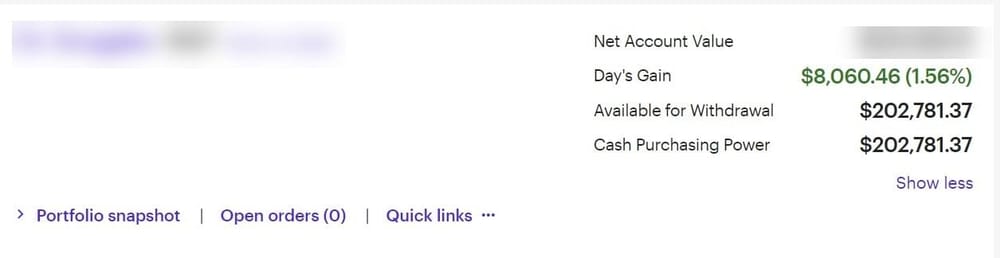

(checkout my daily returns from Sept 28 of 2022)

They can fuck right off with their single-digit returns.

This book and system is my personal way of striking back at a system that just WASTES peoples’ money.

It’s a bit of a legacy project for me.

The third reason - is because I’ve moved to Thailand so I can enjoy beaches and sunshine.

I don’t want to be a financial Guru.

I just want to take selfies with bundles of bananas and enjoy a Pina Colada in paradise while doing my part to screw over financial advisors.

…Which is just enough money that I can pay a team to keep this website running…

Answer any emails…

And occasionally buy an extra cocktail on the beach.

I’m really just here to get this information out there.

Not make a huge profit on a $27 dollar book.

But Ryan...

Even if you’re right… I don’t want to risk all my money on a strategy from a guy I just met on the internet.

And if you’ve never managed your own money before…

It can all be a bit overwhelming.

So let me make a suggestion instead.

(I’m not allowed to give financial advice for legal reasons… but I CAN make suggestions)

Right now, you realistically have 3 options:

– OPTION #1 –

The Super Conservative

Buy my $27 strategy, and then use a demo account to open up a pretend stock portfolio.

This is EXACTLY how I got started.

I used pretend money in a ‘demo account’ (which you can get super easily for free) to play around and refine my filters all those years ago.

But it’s a super easy (and cheap) way for you to experiment with this strategy on your own…

And you can pick any amount of pretend money you want to trade with.

(I’d recommend using the same amount as you have to invest so the numbers are all similar)

The only downside is that WHEN this strategy works for you, you’re going to wish you’d used real money from day 1.

– OPTION #2–

The Low Risk

Buy my $27 strategy, and then use a small amount of your own money to open up a real portfolio.

Use just enough money that you can actually make a reasonable return.

And then invest more money once you’re confident in your ability to buy stocks at the right time!

(again, I can’t give financial advice, but this is what I’d recommend that a friend do)

– OPTION #3 –

Balls Deep High Roller

Buy my $27 strategy, and then use a large amount of your own money to open up a real portfolio.

Throw everything you have, including your house, car and children into the mix!

I don't recommend this but some of my clients have done it and it's worked out well!

ALL three options are better than continuing to let financial advisors make you miserable returns WHILE STEALING your future wealth.

If you really want to make significant returns on your money so that your money can work FOR YOU and build wealth while you sleep…

You need to be managing your own money!

And of all the things I’ve done or tried…

THIS strategy is easily the most effective and time-efficient stock-buying strategy I’ve ever used.

I'll Give You The WHOLE System For $27

And in case you're thinking of putting this off...

Here are 2 things to consider...

(That’s the official number anyways - the REAL number is likely closer to 12 or 18%)

So if your portfolio only makes you 5% per year…

2022 just set you back TWO years of profits!

That means you have effectively 10% less money this year than you did last year.

POTUS has inflated that 10% right out of your pocket.

And right now, most financial managers are scrambling just to break even.

Laughing.

I’m on my way to hit ANOTHER 66% INCREASE this year… so the 9% inflation really doesn’t mean much to me.

And you could be laughing at inflation too - IF you had access to this system.

The SECOND THING is that I’m not going to be able to keep this offer up forever.

Paying someone to keep this website alive has gotten more and more expensive.

Web costs are up more than ever, and frankly if it becomes too much more of a hassle…

I’m just going to shut the whole thing down and go back to my beach.

SO IF YOU WANT IN…

And you want access to the kind of 5-minute stock buying strategy that will make your financial advisors GREEN with envy…

Then don’t wait, because I really don’t know how much longer we’re going to be able to keep this thing on the internet.

How to quickly and easily set up a 401K and trading account.

How to rapidly find 'bounce back' stocks in just 5 minutes per day.

How to virtually guarantee an immediate 22% return (or higher depending on your tax bracket) by simply managing your own money.

How to pay yourself if you're self employed, so you can invest with pre-tax money AND match your own contribution to a 401K.

Why you should NEVER keep more than $1,000 in a bank account at once (and where you should keep the rest of your money instead so that it's safe and easily accesible).

How to stay ahead of inflation so Uncle sam doesn't steal your hard-earned cash.

And so much more!

(which I can’t do for legal reasons)

So if you want access to the exact system that made me a millionaire in 5 years in just 5 minutes per day…

And to take control of your finances learning how to easily invest pre-tax dollars…

Then all you have to do is click the button below and fill out the order form on the next page.

I’ll see you inside,

Ryan

I'll Give You The WHOLE System For $27

P.S. In case you're one of those people who just scrolls to the bottom to read the summary...

I’m going to give you access to the exact 5-minute stock trading system I’ve used to make a 66% increase on my investments in the market, every year for the past five years.

You’re going to discover:

How to quickly and easily set up a 401K and trading account.

How to rapidly find 'bounce back' stocks in just 5 minutes per day.

How to virtually guarantee an immediate 22% return (or higher depending on your tax bracket) by simply managing your own money.

How to pay yourself if you're self employed, so you can invest with pre-tax money AND match your own contribution to a 401K.

Why you should NEVER keep more than $1,000 in a bank account at once (and where you should keep the rest of your money instead so that it's safe and easily accesible).

How to stay ahead of inflation so Uncle sam doesn't steal your hard-earned cash.

And so much more!

Without one of those thieves (I mean financial advisors) steal from you.

This proven method TRULY takes only a few minutes per day…

And spending MORE time than that is actually useless.

And if you miss a day or two?

No problem.

Just check back the next time you take your morning 💩

AND I WANT TO MAKE THIS CLEAR:

When you get access to this system… I make NOTHING on your stocks.

This is NOT a proprietary software…

This is NOT a communal fund…

This is NOT an ‘investment opportunity’...

Although it is one HELL of an opportunity.

This is just a 52 page PDF instant download that reveals the EXACT 5-minute method that’s made me a 66% increase in the markets, every year for the past 5 years.

Without stressing…

Without ‘trading’...

Without letting one of those financial advisor bastards take 2-3% as a fee for only making you 5% on your money.

It’s the step-by-step plan that let my girlfriend turn $15k into a $1,000,000 in a few years with the right stock purchases (and regular contributions)...

And made me a millionaire in 5 years by just spending 5 minutes a day checking my stocks on the toilet each morning.

More importantly!

This does NOT involve penny stocks, crypto, or crazy risks

I’m neither.

Instead, this system depends entirely on rapidly identifying large and proven companies that are established and virtually guaranteed to succeed in the long term…

And then buying them on a ‘bad day’ so you make an immediate return when they recover.

AND IF THAT WASN’T ENOUGH…

I can virtually GUARANTEE A 22% MINIMUM return by managing your own money simply because you’ll be investing your pre-tax income!

(and it’s as easy as completing a quick online application for a 401K account)

So even if you do almost everything wrong… you’ll still end up with a return that is WAY bigger than any financial advisor could ever dream of.

And if that sounds good to you…

Then you can get access to the system TODAY for just a one-time payment of $27

It’s a 52 page E-book that reveals my exact strategies…

The ‘filters’ I use to rapidly search for qualified stocks that are having a ‘bad day’...

The tax strategies to ensure you get instant returns by investing pre-tax income…

And my preferred brokers, accounts, and all the little details in between.

And if you take action TODAY…

You could be managing your money by this time tomorrow.

All you have to do is click the button below.